The emergence of the newspace industry, characterized by the entry of private companies into the space industry, has significantly advanced the development of on-orbit servicing (OOS): any activities carried out upon satellites in orbit by other spacecraft. This progress is largely due to advancements in automation, robotics and navigation technologies that enabled intentional maneuvers to bring a satellite close to another object in orbit for docking or conducting nearby operations. These developments, combined with the miniaturization of components and reduced launch costs, have made OOS more feasible than ever before. However, the level of industry interest and economic viability of such services are subject to several complex dynamics, indicating that bringing OOS to market may be a slow process.

Limited interest in extending the life of LEO satellites

One of the primary motivations for OOS is to extend the operational lifespan of satellites. However, in low Earth orbit (LEO), the low cost of launching satellites has reached a point where the risk and cost of OOS operations do not justify the benefits. It is often more practical and economical to launch new, more advanced satellites rather than prolong the life of existing ones. Furthermore, satellite operators are increasingly enhancing the propulsion capabilities of their satellites, improving autonomy and flexibility, thereby diminishing the need for external support to extend their operational lifespan.

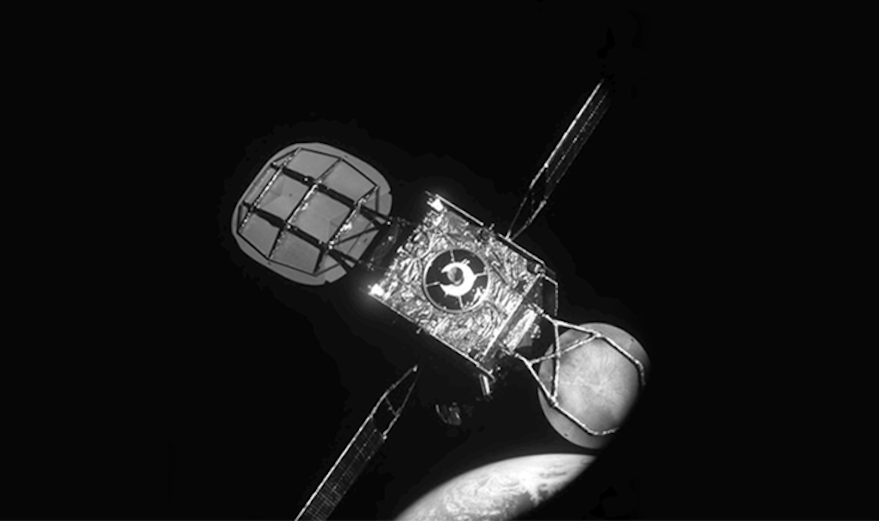

In contrast, extending the life of satellites in geostationary orbit (GEO) offers significant value to operators who face profitability challenges. Northrop Grumman’s Mission Extension Vehicle demonstrated the feasibility and benefit of such services by extending Intelsat 901’s life by five years — a 25% lifespan increase. However, the GEO market is undergoing disruption due to the emergence of broadband megaconstellations in LEO. This shift presents a dilemma for manufacturers who see their order books shrinking, and for OOS providers who rely on GEO for a substantial portion of their revenue. If the adoption of small GEO satellites becomes widespread, launching new satellites might again prove more attractive than servicing existing ones, just as is the case in LEO.

Debris removal: an unclear path to a promising market

The issue of space debris is another potential market for OOS. Governments and space agencies such as those of Europe, the United Kingdom, and Japan are investing in projects to develop demonstrators for debris removal. Constellations in orbit hold significant value for operators, and debris poses a substantial threat to their services. Despite this, the growing propulsion capabilities of satellites, which enable self-deorbiting at the end of their life, reduce the necessity for external debris removal services. Only in cases of propulsion failure would such services be intermittently needed.

Regulatory changes, like the FCC’s $150,000 fine to DISH for poor end-of-life management, indicate a tightening regulatory landscape. However, for regulations to drive demand for end-of-life services, the cost of these operations must be lower than the penalties, which currently seems unlikely. Operators tend to increase their fuel capacity primarily to manage the end-of-life phase of satellites, but this additional fuel could also be used to extend their operational lifespan if an external servicer handles the deorbiting. However, low-cost LEO operators are likely to prefer fleet renewal over service extension.

However, international collaboration could help drive down the costs of OOS to feasible amounts. For example, the recent Zero Debris Charter signed by 12 European countries could foster more collective initiatives among signatories, distributing the costs of achieving debris neutrality by 2030. This collaborative approach could make debris removal services more viable

Uncertain horizon for maintenance and assembly in orbit

While there may be interest in maintaining and assembling spacecraft in orbit, the market is likely to emerge only in the long term, driven by large-scale, expensive infrastructure projects such as new space stations, solar power stations, data centers or scientific satellites. Robotic spacecraft could prove cheaper and less risky than human astronaut intervention, and could mitigate failure risks through regular spacecraft inspection and maintenance. Additionally, in-orbit assembly services could make it possible to develop larger space structures, the sizes of which are limited by current launch vehicle capabilities. However, the development of very large capacity launch vehicles like SLS and Falcon Heavy might ease these design and assembly constraints, diminishing the need for in-orbit assembly services.

The current demand for OOS remains limited, and OOS services will likely emerge following a market consolidation where few service providers conduct on-orbit services primarily supported by governmental institutions, perhaps to maintain operational sovereignty and ensure sustainable activities in space. To succeed, OOS providers must demonstrate their ability to operate with a very low level of risk compared to launching a satellite. Regulations need to evolve, for example to impose fines for poor end-of-life management that are significantly higher than the cost of the service. Additionally, service providers should be able to reduce their service costs, for instance, by using systems capable of performing multiple operations for various clients. Much remains to be done before OOS becomes viable, but recent initiatives and events offer promise that we may unlock the full potential of this market.

Alexandre Corral is an expert in innovation management and market exploration within the space industry, currently leading projects in the consulting firm Alcimed. Over the past eight years, he has conducted in-depth studies in collaboration with satellite operators, space agencies, and service providers, providing a comprehensive and strategic perspective on evolving space markets.