The BEA hugely revised GDI to the downside. Hmm. It seems that voters weren’t fooled.

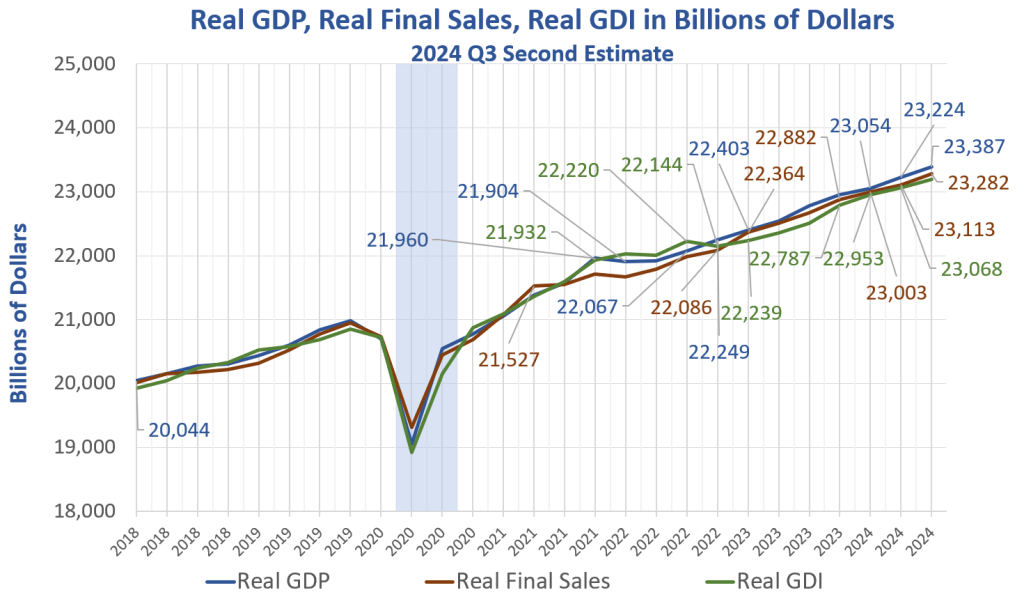

Chart Notes

- Gross Domestic Product (GDP) and Gross Domestic Income (GDI) are two measures of the same thing.

- Income should match products sold, and does over time. But the discrepancies since Covid have been on the wild side.

- Real Final Sales is the bottom-line estimate of GDP. The rest is inventory adjustment that nets to zero over time.

On Wednesday, the BEA released its Second Estimate of GDP and its first estimate of GDI for the third quarter of 2024.

Current‑dollar GDP increased 4.7 percent at an annual rate, or $337.6 billion, in the third quarter to a level of $29.35 trillion, an upward revision of $4.4 billion from the previous estimate.

The price index for gross domestic purchases increased 1.9 percent in the third quarter, an upward revision of 0.1 percentage point from the previous estimate. The personal consumption expenditures (PCE) price index increased 1.5 percent, the same as previously estimated. Excluding food and energy prices, the PCE price index increased 2.1 percent, a downward revision of 0.1 percentage point.

Real GDP, Real Final Sales, Real GDI in Billions

The gap between GDP and GDI is widening again.

Also note the gap between Real Final Sales and GDP. This is inventory adjustment and inventory padding.

Due to Trump tariff threats, importers are likely padding as much inventory as they can before Trump hikes tariffs.

I expect a huge jump in inventories for the fourth quarter.

If buyers don’t show up for this stocked merchandise, merchants will get clobbered holding stuff people aren’t buying.

Updates to GDP

- The second estimate reflects upward revisions to private inventory investment, nonresidential fixed investment, state and local government spending, and residential fixed investment.

- The second estimate reflects downward revisions to exports, consumer spending, and federal government spending. Imports were revised down.

Updates to Second-Quarter Wages and Salaries

- Private wages and salaries are now estimated to have increased $65.0 billion in the second quarter, a downward revision of $91.8 billion.

- Personal current taxes are now estimated to have increased $39.8 billion, a downward revision of $15.5 billion.

- Contributions for government social insurance are now estimated to have increased $7.0 billion, a downward revision of $12.4 billion.

- With the incorporation of these new data, real gross domestic income is now estimated to have increased 2.0 percent in the second quarter, a downward revision of 1.4 percentage points from the previously published estimate. See lead chart.

The BEA explains “Today’s release presents revised estimates of second-quarter wages and salaries, personal taxes, and contributions for government social insurance, based on updated data from the Bureau of Labor Statistics Quarterly Census of Employment and Wages program.”

Mish July 26, 2024: Expect the BLS to Revise Job Growth Down by 730,000 in 2023, More This Year

At the heart of these revisions is a horribly flawed birth-death model used by the BLS. My calculation closely matches an estimate by Bloomberg’s chief Economist.

Mish August 21, 2024: BLS Revises Jobs Down by 818,000 the Most Ever, About 68,000 Per Month

Do I get to say I told you so? My advance estimate a month ago was 779,000 lower. Bloomberg estimated 730,000.

Quarterly QCEW Data Provides More Evidence of BLS Jobs Overstatement

On November 20, I commented Quarterly QCEW Data Provides More Evidence of BLS Jobs Overstatement

My prior comparisons and advance calls suggest we see negative revisions in nonfarm payrolls from 2023 Q2 to 2024 Q2 of well over one million. My initial stab is about 1.2 million to the downside.

The BLS Birth-Death model is seriously messed up an/or the BLS is oversampling large corporations and under sampling small businesses.

The BLS monthly nonfarm payroll reports are consistent garbage.

Reflections on BEA Revisions

If jobs overstated, income is too. And on Wednesday we found out the BEA overstated wages by a massive $91.8 billion from $156.8 billion to $65.0 billion.

This resulted in a downgrade in GDI growth from 3.4 percent growth to 2.0 percent in the second quarter.

It appears the BEA is incorporating BLS garbage into its reports as well. That massive 3.4 percent to GDI in Q2 was fiction as I suspected all along due to QCEW data analysis.

Expect more negative revisions because they are coming.

Lacy Hunt pinged me with this observation: “The economy looks more and more like 2008, when for many the economy appeared to be just fine. Then came the downward revisions. When all was said and done, the NBER determined the cycle peak was December 2007. The deep revisions are continuing just as sixteen years ago.”

Neither of us think this recession will look like 2008 or 2020. It won’t for many reasons, but the revision signs are flying high.

Two Big Economic Shocks Coming

On top of negative revisions, the key driver of job growth, immigration, will end. So will the surge in related government handouts.

For discussion, please see my October 6 post Government Jobs Rose by Nearly 1 Million Unadjusted in Sept, What Going On?

On an unadjusted basis government jobs rose by 984,000. The BLS says jobs rose by 73,000. A reader asked about this.

Also see my November 1 post Nonfarm Payrolls Rise a Mere 12,000 with Government Jobs Up 40,000

Job Stats vs One Year Ago

- Nonfarm Payrolls: +2,173,000

- Employment: +216,000

- Full Time Employment: -1,000,600

Second, a big consumer tax hike is coming assuming Trump does what he says.

So, we have already slowing job growth and now we have a migration shock and a tax hike shock coming just as nearly everyone has given up on the recession idea.

Good luck with that. Voters weren’t fooled, just the economists.

In case you missed it, please see My Thanksgiving Thanks to Followers