There is still a 78.6 percent chance of at least a quarter-point cut in June.

This morning I wrote Hot PCE Inflation Data and Weak Spending Sure to Give the Fed Headaches

There is no good news on inflation or spending in recent data.

And yields on long-term bonds surged. The yield on the 10-year note jumped 11 basis points to 4.25 percent. The yield on the 30-year bond jumped 9 basis points to 4.63 percent.

But the Fed has penciled in two rate cuts this years with the market closer to three, and the market did not change its view.

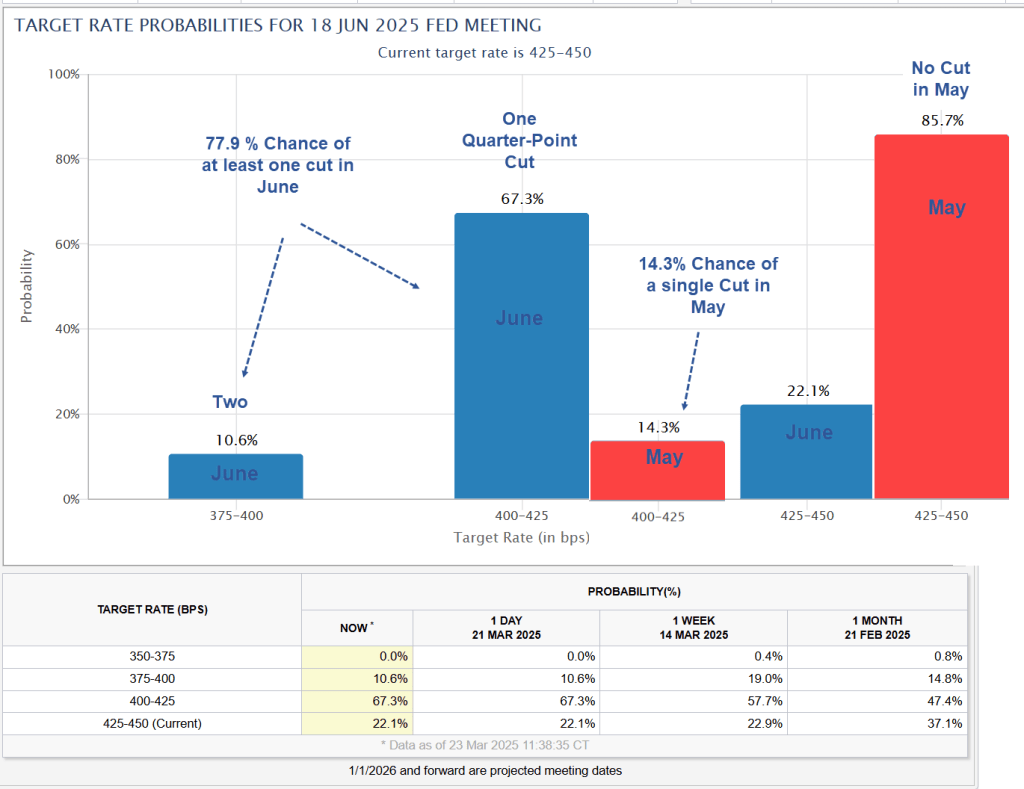

Unfortunately, I failed to capture the above chart yesterday to see the precise change. But I did capture charts on March 23.

Target Rate Probabilities for 2025-06-18 as of 2025-03-23

Six days ago the market saw a 77.9 percent chance of at least one rate cut in June. Now, despite hot inflation, the odds only dropped to 78.6 percent.

Six days ago, the odds of a rate cut for May were 14.3 percent. The odds have actually increased to 18.5 percent.

How to Make Sense of This

If the Fed does cut in June for no reason other than it has penciled one in (this is certainly possible), I would expect long-term yields to rise, and they did.

The other possibility is the market expects a recession sooner rather than later. As for the long bond in this recession scenario, it makes perfect sense for worries over long-term budget deficits.

What to Expect

If the Fed wants to push back on the rate cut idea it will start yapping that way.

If the Fed wants to go along with the “everything is under control” meme, then it will make excuses to cut.

If there is no general consensus, then yapping may be all over the place. In that case, pay attention to Fed Chair Jerome Powell and New York Fed President John Williams and ignore the rest.

Forward Guidance

By the time we get to the June meeting, the Fed will have yapped the market to what it wants to do.

The nonsensical process where yapping matters more than data, we call “Forward Guidance”.

And best of all [sarcasm] the banks get to front-run the yapping.

Is Market Driving Rate Cuts?

No, not really. The Fed jawbones the market with nonsense about inflation expectations, dot plots, and forward guidance.

The market tends to front-run Fed jawboning.

But when the market gets too far in front or behind what the Fed wants to do, a parade of Fed governors starts yapping, generally in-line with what the Fed Chair wants to do.

I have discussed this many times before but let’s do a quick recap.

The Fed Uncertainty Principle

Please consider The Fed Uncertainty Principle written April 3, 2008 before the collapse of Lehman Brothers and Bear Stearns.

Does the Fed Follows the Market?

Most think the Fed follows market expectations.

However, this creates what would appear at first glance to be a major paradox: If the Fed is simply following market expectations, can the Fed be to blame for the consequences? More pointedly, why isn’t the market to blame if the Fed is simply following market expectations?

This is a very interesting theoretical question. While it’s true the Fed typically only does what is expected, those expectations become distorted over time by observations of Fed actions.

If market participants expect the Fed to cut rates when economic stress occurs, they will take positions based on those expectations. These expectation cycles can be self-reinforcing.

The Observer Affects The Observed

The Fed, in conjunction with all the players watching the Fed, distorts the economic picture. I liken this to Heisenberg’s Uncertainty Principle where observation of a subatomic particle changes the ability to measure it accurately.

The Fed, by its very existence, alters the economic horizon. Compounding the problem are all the eyes on the Fed attempting to game the system.

A good example of this is the 1% Fed Funds Rate in 2003-2004. It is highly doubtful the market on its own accord would have reduced interest rates to 1% or held them there for long if it did.

What happened in 2002-2004 was an observer/participant feedback loop that continued even after the recession had ended. The Fed held rates rates too low too long. This spawned the biggest housing bubble in history. The Greenspan Fed compounded the problem by endorsing derivatives and ARMs at the worst possible moment.

In a free market it would be highly unlikely to get a yield curve that is as steep as the one in 2003 or as steep as it was just weeks ago when short term treasuries traded down to .21%.

The Fed has so distorted the economic picture by its very existence that it is fatally flawed logic to suggest the Fed is simply following the market therefore the market is to blame. There would not be a Fed in a free market, and by implication there would be no observer/participant feedback loop.

Fed Uncertainty Principle: The fed, by its very existence, has completely distorted the market via self-reinforcing observer/participant feedback loops. Thus, it is fatally flawed logic to suggest the Fed is simply following the market, therefore the market is to blame for the Fed’s actions. There would not be a Fed in a free market, and by implication, there would not be observer/participant feedback loops either.

Corollary Number One: The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

Corollary Number Two: The government/quasi-government body most responsible for creating this mess (the Fed), will attempt a big power grab, purportedly to fix whatever problems it creates. The bigger the mess it creates, the more power it will attempt to grab. Over time this leads to dangerously concentrated power into the hands of those who have already proven they do not know what they are doing.

Corollary Number Three: Don’t expect the Fed to learn from past mistakes. Instead, expect the Fed to repeat them with bigger and bigger doses of exactly what created the initial problem.

Corollary Number Four: The Fed simply does not care whether its actions are illegal or not. The Fed is operating under the principle that it’s easier to get forgiveness than permission. And forgiveness is just another means to the desired power grab it is seeking.

The Fed Uncertainty Principle is still my all-time favorite post.

Related Posts

March 27, 2025: Second Massive Wave of Imports Shows More Tariff Front Running

The advance import-export data for February is another doozie. Three charts.

March 27, 2025: US Debt Will Grow to a Staggering 156 Percent of GDP by 2055

If Congress extends the TCJA tax cuts with no offsetting savings, the deficits will surge.

March 28, 2025: GDPNow Nowcast Takes a Steep Dive Into Negative Territory, What Happened?

Another blast of imports and a poor spending report impacted the Nowcast.

If your base case is stagflation, then this post, including the above links makes a nice case.

I am not convinced of that outcome, however.

No one really knows what Trump will do or the ultimate impact of a huge wave of tariffs if he goes ahead.

My base case is a slowing economy and recession. Enough to override the inflationary impacts of tariffs? I think so, but remain unconvinced.