Insurance, repairs, and maintenance costs are up for both homes and autos. Some homeowners are skipping home insurance. What’s going on and who is to blame?

Auto and Home Chart Notes

- All data via St. Louis Fed FRED repository, index levels all set to 1015=100

- CPI components where found and closest equivalent when not

- Case Shiller Home Price Index: S&P Dow Jones Indices LLC, S&P CoreLogic Case-Shiller U.S. National Home Price Index

- Maintenance and Repair of Dwellings: OECD Main Economic Indicators

- Homeowners Insurance: PPI Premiums for Homeowner’s Insurance

- New and Use Motor Vehicles: CPI New and Used Motor Vehicles in U.S. City Average

- Motor Vehicle Maintenance and Repairs: CPI Motor Vehicle Maintenance and Repair in U.S. City Average

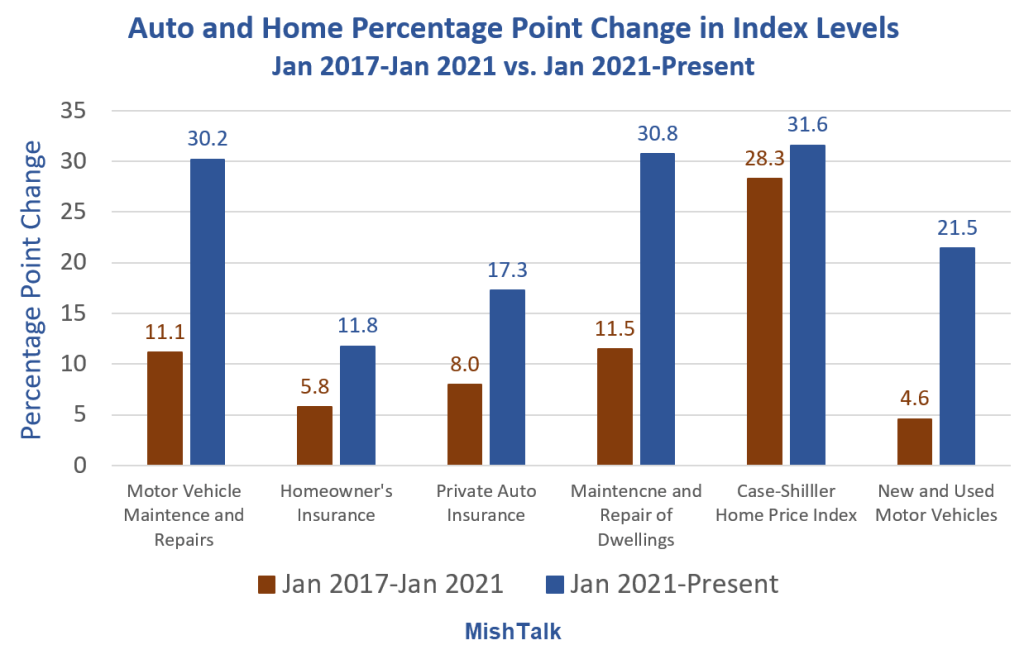

Auto and Home Index Level Percentage Point Changes

- Case-Shiller Home Price Index: Trump 28.3% vs Biden 31.6%

- New and Used Cars: Trump +4.5% vs Biden 21.5%

- Homeowner’s Insurance: Trump +5.8% vs Biden 11.8%

- Private Auto Insurance: Trump +8.0% vs Biden 17.3%

- Maintenance and Repair of Dwellings: Trump 11.5% vs Biden 30.8%

- Motor Vehicle Maintenance and Repairs: Trump 11.1% vs Biden 30.2%

The Hidden Costs of Homeownership Are Skyrocketing

The Wall Street Journal comments The Hidden Costs of Homeownership Are Skyrocketing

Darren Gondry has owned his four-bedroom home near a golf course in Louisville, Ky., since 2004. He and his wife, Lori Gondry, paid off their primary mortgage in 2021.

That hasn’t stopped other bills associated with homeownership from piling up. Their home insurance costs have risen 63% in two years. Their property taxes, utility costs and homeowners’ association fees have risen in recent years, too.

“I was so sticker-shocked,” Gondry said of the mounting home-cost increases. “I fear they’re here to stay.”

Homeownership affordability fell to its lowest level since the 1980s last year as mortgage rates reached a 23-year high and home prices set new records.

Property taxes and home-maintenance costs are climbing in much of the country. Non-mortgage costs including property taxes, maintenance, utilities and insurance make up more than half of homeowners’ overall costs, according to a 2022 analysis by Fannie Mae economists.

Worst of all, home insurance premiums are soaring. Rates rose by more than 10% on average in 19 states in 2023 after a series of big payouts related to floods, storms, wildfires and other natural disasters across the U.S., according to an Insurance Information Institute analysis of data from S&P Global Market Intelligence.

Plenty of homeowners are having to stretch financially to meet these home-related expenses. Nearly one in five said they couldn’t afford a $500 emergency repair without going into credit-card debt, according to a February online survey of 1,000 homeowners by tech company Clever Real Estate, while 42% said they’ve skipped home repairs or maintenance because of the cost.

Home maintenance fees have risen. It cost an average of $6,663 a year to maintain a home in the fourth quarter of 2023, up 8.3% from a year earlier, according to home-improvement tech company Thumbtack.

In Manhattan, one of the country’s priciest real-estate markets, typical home values fell 8.9% in February from a year earlier, according to Zillow. But the monthly maintenance fees for recently sold co-ops rose 62% from the first quarter of 2020 to the first quarter of 2024, and condo fees rose 45% in the same period, according to appraisal firm Miller Samuel.

In Charlotte, N.C., the average property tax rose 31.5% from 2022 to 2023. In Indianapolis it was up nearly 19%.

Insurify expects average home-insurance costs to rise by more than 10% in eight states this year, including Louisiana, Maine and Michigan.

Steve Kissee listed two Louisiana houses for sale last year, an inherited property and a vacation home.

Kissee is also struggling with insurance costs for his primary home in New Orleans. He received a renewal quote for wind and hail insurance last year for about $31,000, up from a $3,200 premium the year before. He switched to the state’s insurer of last resort for about $7,900 after replacing his roof. His monthly payment for taxes and insurance is higher than the principal and interest payment on his mortgage, he said.

In Colorado, the 2021 Marshall Fire that swept through the suburbs between Denver and Boulder is still boosting insurance costs in that state. Insurance broker Michael McCarron said many of his clients’ home-insurance bills are rising 20% to 40% a year.

Those who live in flood zones, hurricane zones, or fire zones have seen their rates rise 50-100 percent or more. A quote from $3,200 to $31,000 is shocking.

Ask anyone in a hurricane zone, anyone in school, and anyone who buys their own health insurance what their inflation rate is.

The BLS averages all of this. Economists wonder why so many people are angry.

Assessing the Blame

Neither Trump nor Biden handled Covid well, but Biden was an outright disaster.

The third and final fiscal stimulus under Biden was totally unwarranted and unleashed a huge amount of inflation (see fiscal stimulus chart below).

It’s important to note that Trump wanted the fiscal stimulus that Biden got, but Congressional Republicans delivered a much smaller package.

Trump started eviction moratoriums, but Biden kept them too long and fought with the Supreme Court to keep them going longer. The same applies to student aid.

The fiscal stimulus was massive and unwarranted as were the lockdowns. Biden and Democrat governors kept lockdowns and school cancellations going long after it was easily apparent they were no longer doing any good.

For some of the supply chain problems, no one is to blame explicitly, but the fiscal stimulus exacerbated the problems.

Fiscal Stimulus

Consumer Price Index

Prices had already started to soar before the third and largest round of stimulus.

Role of the Fed

The Fed’s role in all of the housing components is massive. Home prices were already soaring, up 28 percent in the Trump years.

The Fed (economists in general) view home prices as a capital expense, not a consumer expense. Thus home prices are not in the CPI nor in the PCE (Personal Consumption Expenditures) measure of inflation. The latter is the Fed’s preferred measure.

This is a serious ongoing economic mistake by the Fed. The Greenspan Fed and the Bernanke Fed both ignored home prices. Asset bubbles brewed, culminating in the Great Recession.

Powell made the same mistake. However, because there were no liar loans this time, the result is people are trapped in their homes unwilling to trade a 3.0 percent mortgage for a 7.0 percent mortgage.

Compounding the inflationary problem, everyone with an existing mortgage refinance at 3.0 percent, This put extra money in their pockets every month fueling consumption.

The Fed’s QE also created an asset bubble in stocks, also fueling consumption. Those wanting to buy a house are trapped out by soaring prices and high mortgage rates.

The Fed’s Big Problem, There Are Two Economies But Only One Interest Rate

I described the Fed’s role on February 20 in The Fed’s Big Problem, There Are Two Economies But Only One Interest Rate

And as a direct result of soaring home prices, insurance and maintenance costs had to rise. The only surprise is the lag in which that happened.

Some of the lag is due to regulators prohibiting insurers to raise prices.

Proposition 103 Backfires, State Farm to Cancel 72,000 California Policies

Citing wildfire risk, State Farm will not renew policies on 30,000 homes and 42,000 business in California.

On March 26, I noted Proposition 103 Backfires, State Farm to Cancel 72,000 California Policies

Caping insurance rates has the same effect as capping rents.

The former leads to an exodus of insurers. The latter lead to an exodus of builders and repairs.

What About Autos?

The push to EVs is part of the reason costs are up (manufacturers had huge capital expenditures but sales have been poor). A record UAW contract also played in rising prices as did a chip shortage.

Biden had a direct role in the UAW contract (Biden was on the Picket Line) and 100% of the role of forcing manufacturers to build EVs before the industry and infrastructure was ready.

The cost of vehicles is up, so the cost of insurance is up.

Whose Job Is It?

Trump, Biden, and Congress all played a role. Biden pressed for all the stimulus and got it. So he gets the credit, or in this case more of the blame, than Trump.

But in assessing the blame we must also factor in responsibilities.

Inflation is the Fed’s direct responsibility. The Fed kept QE going way too long. It slashed rates creating a housing bubble (albeit one of a different flavor), and an asset bubble in stocks.

Powell repeated the mistakes of the Greenspan and Bernanke Fed and on top of it failed to understand, then even see (when it was obvious to the world), what three rounds of fiscal stimulus would do.

The Fed also missed the transition from goods inflation to services inflation. And on the Fed’s watch we had the failure of three banks because the Fed failed to spot obvious speculation by banks in long-dated treasuries.

It doesn’t get more pathetic than that.

Politically speaking, Biden wants credit for reducing the rate of inflation that he and the Fed are most responsible for.

It doesn’t work that way. Biden deserves no credit and polls show people don’t give him any.